3rd pillar pension funds is an attractive option if you want to accumulate independently. It is a personal account in pension funds to save and invest for the future. Both you and your family members or employer can pay contributions to this fund.

If you participate in all three pillars, your future income can be 70-80% of your pre-retirement income instead of 30% (which will happen if you choose only SODRA pension) or 50% (SODRA and 2nd pillar pension).

The State offers incentives for those who choose voluntary accumulation. It offers a personal income tax benefit – a possibility to recover up to €300 a year!

3rd pillar pension funds are attractive because of their flexibility – you decide on the amount of money, how often and in how many funds you want to accumulate, as well as how and when to receive payments.

Sign up for a consultation

Thanks to a professional team, your assets are constantly invested in search of the best risk-return ratio. You can achieve your investment goals by choosing from five INVL 3rd pillar pension funds that differ in their risk, fees and expected return. The longer you invest, the more assets you can expect to accumulate.

If you pay contributions to a 3rd pillar pension fund for yourself, your spouse or children, you can get up to €300 a year refunded. The maximum amount of contributions to which the PIT exemption (20%) is applied is €1,500. More about the PIT benefit read here.

All assets accumulated in a 3rd pillar fund are inheritable. Therefore, everything you accumulate belongs to you and your loved ones. You can also choose the method of disbursement that is best for you.

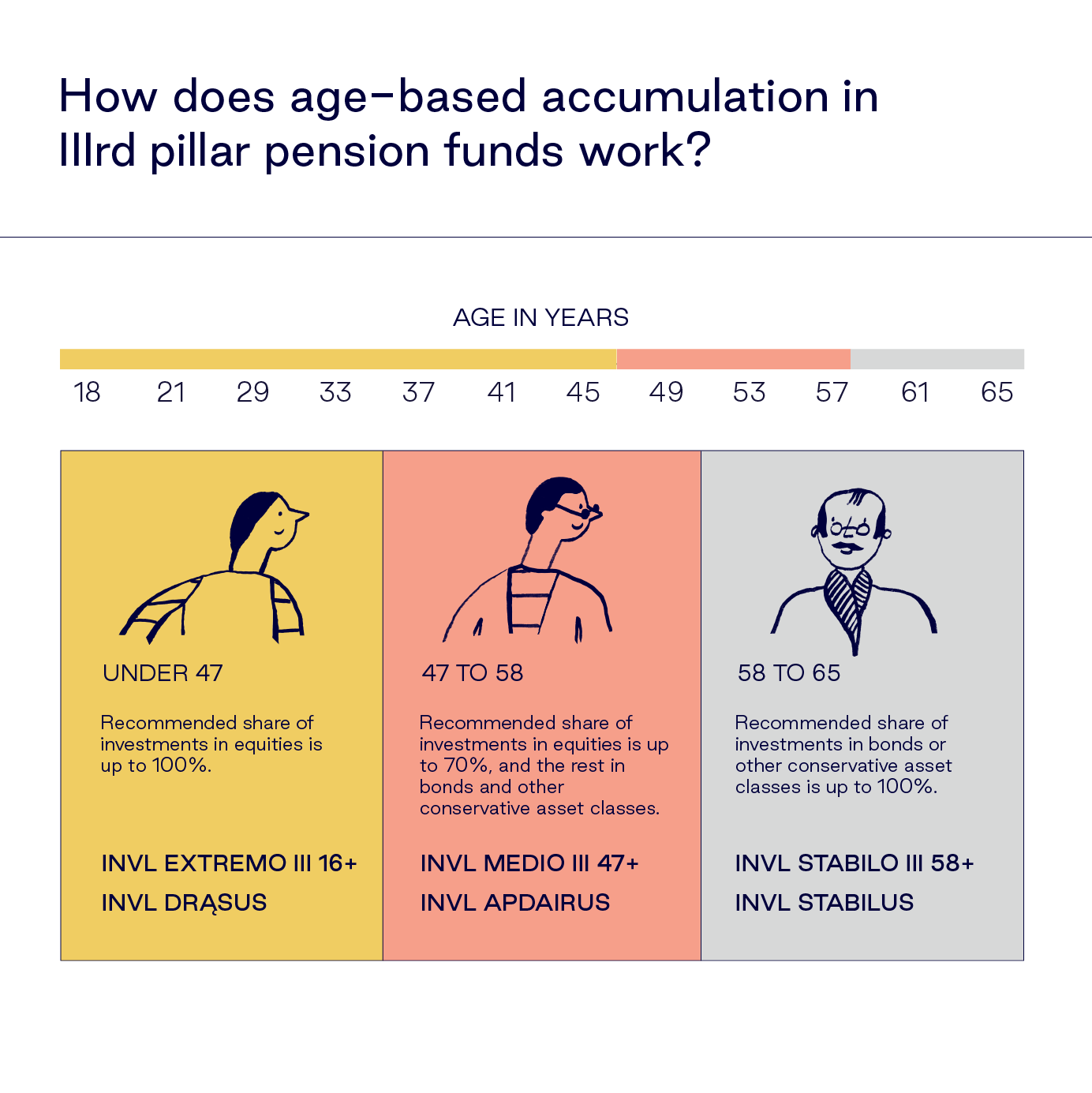

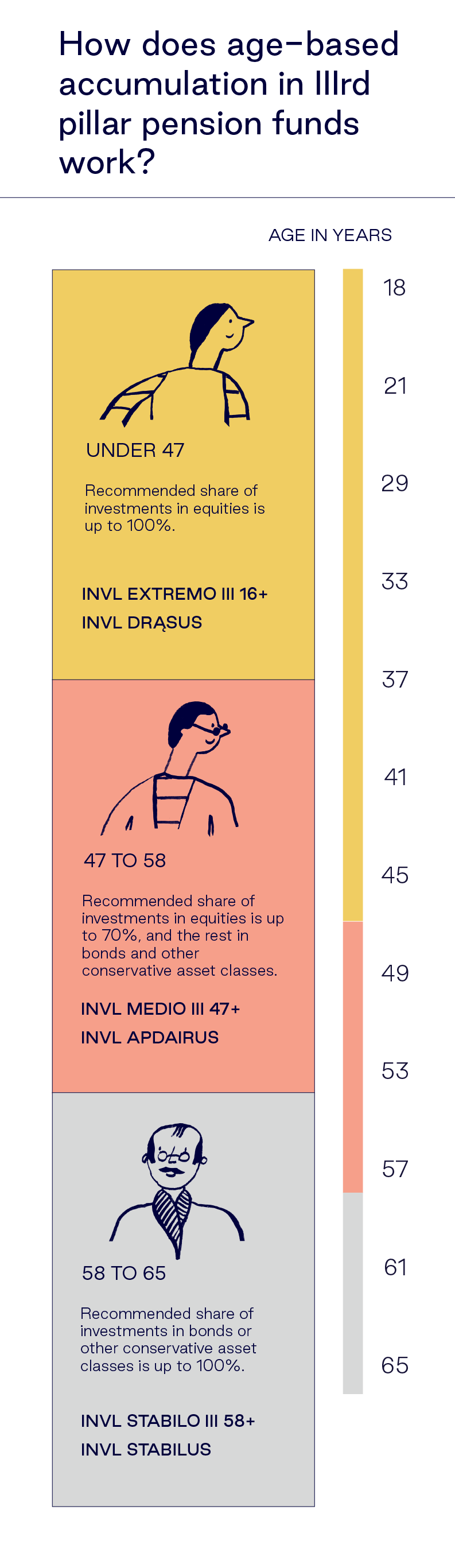

Choose the right fund for you according to your age. Keep in mind that contributions to the pension account can also be paid by your relatives or employer, so discuss it with them in advance.

You can sign a third pillar pension agreement at the INVL office or online. In the INVL self-service portal, you can sign a pension agreement in just a few minutes, using your Smart-ID, mobile signature or photo identification.

Good results can be achieved if contributions to the pension fund are transferred periodically (for example, every month). Also, don’t forget to plan how much money you can set aside for savings every month – the recommended amount is at least 10-15% of your income.

The earlier you start, the more you accumulate. By investing longer, you are likely to earn more. Why? Everything comes down to the compound interest effect: the interest is earned not only on the amount contributed to the fund, but also on the interest earned. In other words, your assets in the fund consist of contributions, interest and interest-on-interest. The longer you accumulate, the bigger amount you have. Of course, markets can rise and fall, but with long accumulation market fluctuations level off.

For example, for Agnė, whose assets had been “employed” for 20 years, every euro earned €0.71. Inga had been investing for 40 years, so every euro she invested earned her €2.18. That’s even three times more!

Although the 3rd pillar allows you to pay contributions of the desired amount at your convenience, if you commit to regular accumulation, you will accumulate assets faster, invest more and have more assets in the 3rd pillar pension fund. Here is a tip for you – take advantage of the e-invoice where you can set the date on which the funds are debited, e.g. after you get paid.

It is easier to save when you get some extra income (e.g. a bonus or a raise). You can also transfer this money to a 3rd pillar pension fund and reach your target amount faster.

Tough competition for labour force makes companies increasingly interested in long-term motivation, including supplementary accumulation for employee’s pension. Employees themselves can also initiate pension accumulation with their employer. Contact INVL and we will tell you more about pension accumulation with your employer.

Log in to the INVL self-service portal, where you will find your messages and always see how much assets you have accumulated. Find out if your contributions are enough for the pension you want. Also, remember that if markets have been fluctuating and the fund’s return has been negative for some time, long-term accumulation will likely smooth out market volatility. This means buying at a good price, thus earning more in the long run as markets recover. If you have any questions, you are always welcome to consult us.

According to the data of the Bank of Lithuania for the first quarter of 2022,

INVL 3rd pillar pension funds were among the leaders

in terms of the average annual return in the last 5 years, in 3 out of 5

categories of pension funds.

Learn more

Accumulate in 2nd pillar pension funds and take advantage of a higher State’s incentive, which is over €216/year for participation in maximum accumulation.

II pillar pension

For optimal return on investment, you should choose a 3rd pillar pension fund based on your age. Younger people are advised to choose funds that invest more in equities, while older people choose funds with a bigger percentage of bonds and a smaller percentage of equities.

So when you reach a certain age, you should change the fund to a less risky one. Check which pension fund corresponds to your age to ensure effective management of your assets and investments for retirement.

People who receive income pay personal income tax (PIT) to the State. Those who accumulate in 3rd pillar pension funds and are permanent residents of the Republic of Lithuania may get part of the PIT refunded by submitting their tax returns. You can also reinvest this State’s incentive, thus increasing the assets that are “employed” in pension funds.

The benefit applies to contributions to 3rd pillar pension funds that you pay for yourself, your spouse or children up to the maximum amount of €1,500, which does not exceed 25% of taxable income. You can get refunded 20% of this paid amount, which is up to €300 a year! All you have to do is submit your tax returns to the State Tax Inspectorate.

Depending on the fund’s investment strategy, pension funds managed by INVL invest in equities and other riskier asset classes (such as real estate or other alternative assets), as well as in bonds. While participants are young (under 47), it is recommended to keep up to 100% investments in equities and risky assets, then reduce their proportion by investing in bonds. Although the value of equities is more volatile, over the long run they allow you to earn more. The risk level of investing in bonds is lower and reduces the fluctuations in the value of accumulated assets as participants approach their retirement age.

When investing in equities, INVL is looking for opportunities on a global scale in order to replicate the return on equity worldwide as effectively as possible and thus grow the assets of participants in their pension funds. In addition, up to one-fifth of these investments go to the Baltic States, as well as Central and Eastern Europe, where we aim to earn higher-than-global returns. Meanwhile, in funds where participants are approaching the retirement age, we aim to preserve the accumulated assets and protect them from inflation, thus they are dominated by direct investments in bonds.

This investment model allows us to ensure a very wide range of equity investments and use undervalued companies or real estate in our region, while investing in bonds directly is more efficient compared to investing through bond funds. You can find the structure of each pension fund in their reports and reviews.

The purpose of 3rd pillar pension accumulation is to save money until retirement. Your management company can set the minimum period of participation in a pension fund. To take advantage of the personal income tax benefit and not pay personal income tax on the amounts that are paid out, you must accumulate for at least five years and withdraw money from the pension funds no earlier than five years before the age established for receiving a state social insurance pension. Read more about payouts from 3rd pillar pension funds here.

You can pay contributions to a 3rd pillar pension fund by yourself or have them paid by your family members or employer. The most convenient way to pay contributions is via e-invoice. E-invoice is a convenient, secure and time-saving way to pay contributions to your 3rd pillar pension fund account.

Subscribe to the newsletter and receive useful information on retirement savings and tips on financial management.

By clicking “Subscribe”, you agree to receive INVL Asset Management news and information about our services and products at the e-mail address provided. In accordance with the company’s privacy policy, this data will be stored for one year.

While participating in a 3rd pillar pension fund, you will be required to pay the fees specified in the rules of the respective fund. The money accumulated in a pension fund is invested according to the investment strategy specified in the rules of the relevant pension fund. When saving in pension funds, you assume the investment and investment-related risk. The value of a pension fund can go both up and down, and you can get back less than you invested. Past performance of a pension fund does not guarantee the same results and profitability in the future. Past performance is not a reliable indicator of future results. When seven or fewer years remain before retirement, consider investing in a conservative investment pension fund (INVL STABILO III 58+/INVL Stable).

Before you make an investment decision, assess all the risks associated with the investment yourself or with a help of investment consultants. Carefully read the rules of the pension fund, which are an integral part of the pension accumulation agreement.

A fund participant may choose from the following forms of pension payment: a lump sum, periodic payments in instalments (conversion of a portion of fund units in the pension account into money to be paid out at regular intervals) or purchase of an annuity from a life insurance company.

All the information presented is of a promotional nature and cannot be construed as a recommendation, offer or invitation to accumulate assets in pension funds managed by INVL Asset Management. The information provided here cannot serve as a basis for any subsequently concluded agreement. Although this information of a promotional nature is based on sources which are considered to be reliable, INVL Asset Management is not responsible for any inaccuracies or changes in the information, or for any losses that may incur when investments are based on this information.

![]()

INVL and Šiaulių bankas merged their retail services as of 1 December 2023.

Please select Your topic on SB.lt webpage.

![]()

INVL and Šiaulių bankas merged their retail services as of 1 December 2023.