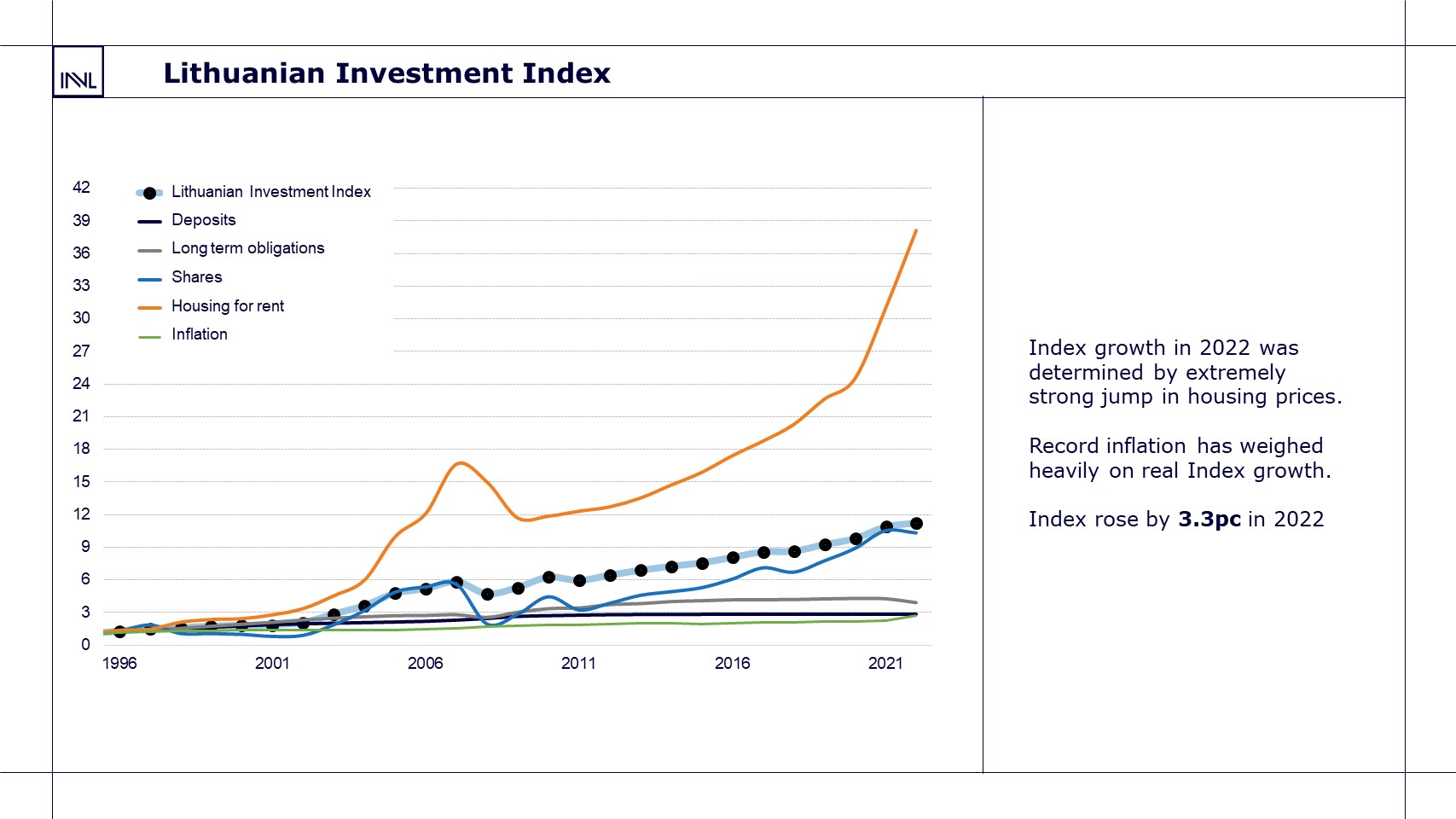

The Lithuanian Investment Index increased 3.3% in 2022 despite a war, a tense situation in the energy market and rising interest rates. The growth was mainly due to a major surge in housing prices. Record inflation, however, reduced the growth of the index in real terms.

The index has risen every year for the last 11 years, doubling over that period. And since its calculation began in 1996, the index has increased more than ten-fold. The Lithuanian Investment Index, which is compiled by the INVL investment management and life insurance group, captures the annual returns on the country’s main asset classes, which are weighted equally: stocks, bonds, rental housing, and deposits.

“Despite the circumstances affecting the world’s economy, Lithuania’s too, the Lithuanian Investment Index rose for an eleventh straight year, and that means that money invested in Lithuania last year earned a return. But different asset classes fare differently at different times, which once again confirms that diversification is the key to getting the most out of investments,” says Vaidotas Rūkas, the Head of INVL’s Investment Management Division.

Growth was driven by a surge in housing prices

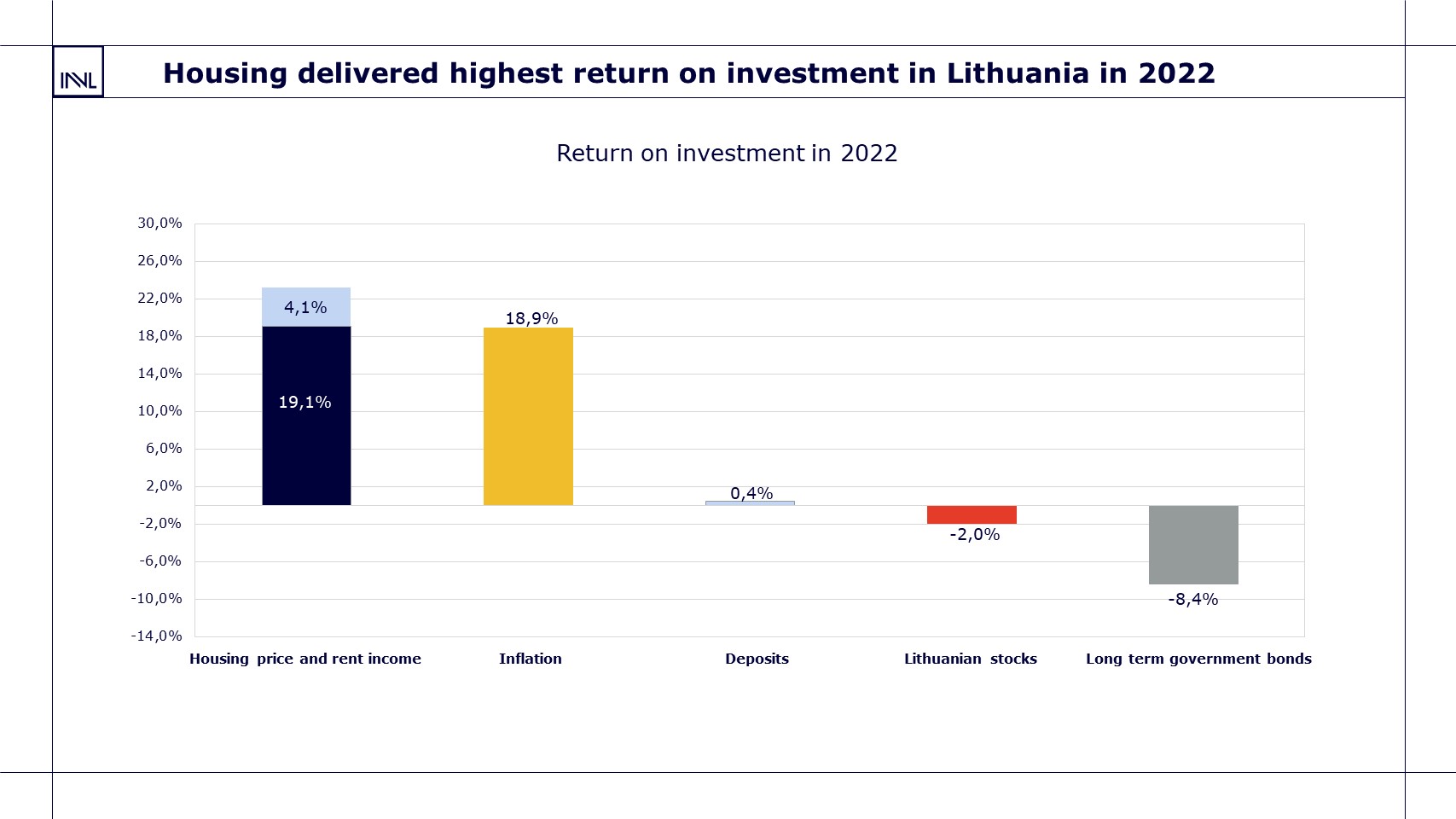

Last year, as in 2021, the biggest factor in the growth of the Lithuanian Investment Index was the return on investments in housing. Housing prices grew 19.1% and rental income added another 4.1% to that return. So investments in housing generated the biggest return for a second year in a row. To compare, in 2019 and 2020 it was Lithuanian stocks that brought the biggest return.

Last year saw a correction in the global stock market. Global equities were hit the hardest, falling 17.9%. The latter part of the year was better for the European stock market, which ended the year down 9.9%. Lithuanian stocks dropped just 2% in 2022, significantly more slowly than their Western European or global counterparts.

In any case, the average long-term annual return on the European, global and Lithuanian stock markets for the past decade and the last 27 years is substantial and well above inflation.

2022 was an atypical year for bonds. Rising interest rates negatively affected bond prices, and as a result returns on long-term bonds were significantly negative. The return on Lithuanian long-term bonds was -8.4% last year. In comparison, the return on US 10-year bonds was -17.8% and that on 10-year bonds in Germany, which is considered one of the safest countries, was -18.9%. It should be recalled that the average annual return on Lithuanian and other developed countries’ bonds over the last decade has been approximately 0 to 0.2%.

Interest rates on deposits in Lithuania have also only averaged 0.2% over the past decade. The average long-term return on this asset class since 1996 fell to 3.9%.

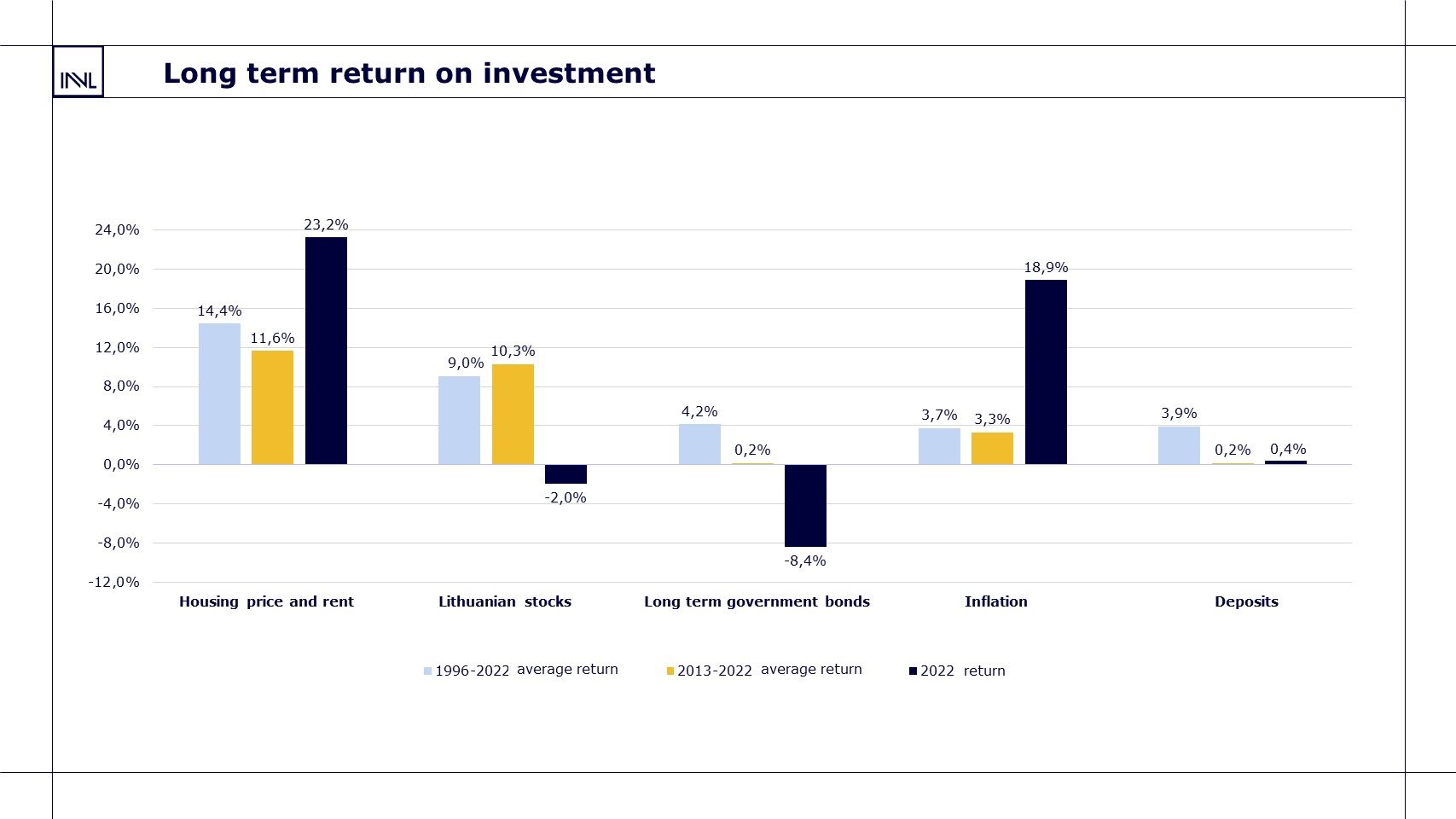

Most money is where returns are lowest

The investments in Lithuania with the highest returns over the long term, both since 1996 (14.4% on average) and over the last decade (11.6% on average), are those in real estate. Lithuanian stocks are not far behind, with a double-digit average annual return for the past decade (10.3%) and a 9% average return since 1996.

These investments have significantly outpaced inflation, which has averaged 3.3% annually since 2013, even taking last year’s record 18.9% jump in prices into account.

The average return on Lithuanian long-term bonds between 2013 and 2022 was 0.2%, and the return on deposits was also 0.2%. Note that the return on deposits, which had been near to nil for the past five years, rose last year to 0.4% amid a sharp increase in interbank interest rates.

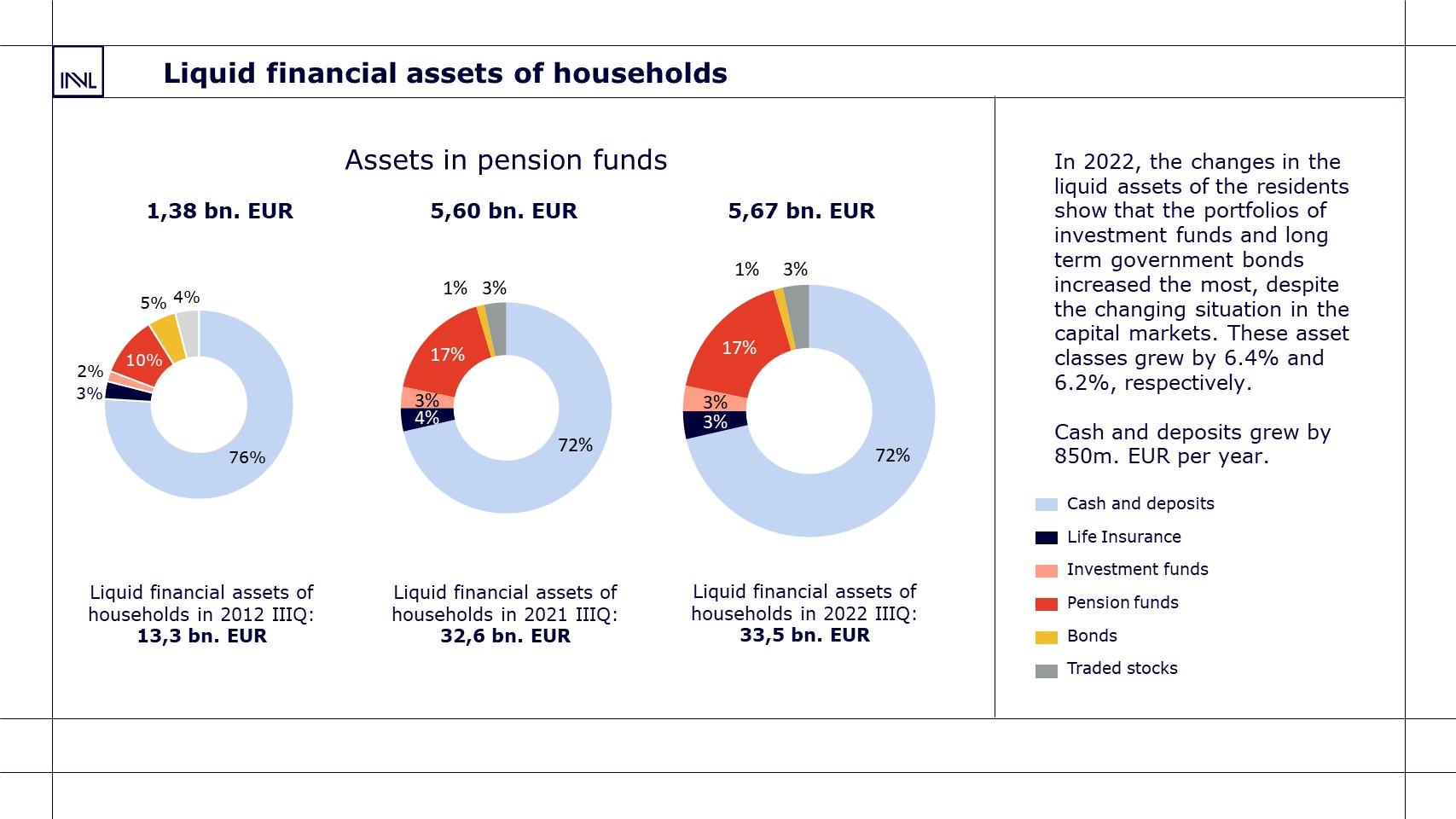

“Even though deposits and cash do not produce returns, they still account for 72% of households’ liquid financial assets. Last year alone, they increased by EUR 850 million. We can at least take comfort from the fact that over 10 years, the proportion of money and deposits has fallen by 4 percentage points, while the proportion of assets people hold in pension funds has increased by 7 percentage points. If in 2013 people held EUR 1.38 million in pension funds, today the figure is EUR 5.67 million, and the proportion of these accumulated assets has grown the fastest, both due to the peculiarities of Lithuania’s pension system and to significant returns on investments. Although 2022 was a negative year for capital markets, historical data show that over the long term, pension fund returns exceed inflation and protect purchasing power,” Vaidotas Rūkas notes.

Outlook for the different asset classes

It would be no surprise to see changes in the rankings of asset class returns in 2023. Lithuanian government bonds, which were the biggest losers in 2022, can be expected to yield an annual 3.5% to 4.5% this year. That has not happened for a long time. Consequently, interest rates on deposits should gradually converge towards the level set by the European Central Bank.

Meanwhile, as interest rates rise and demand for housing weakens due to diminished affordability, housing prices may not just stabilise but could even see a correction. Still, what will most affect prices is the situation on the labour market. Strength in terms of both employment numbers and wages would help to cushion a fall in housing prices.

Lithuanian stocks may fluctuate in the short term due to market uncertainty and changing consumer sentiment, but given the country’s sustained economic growth, the long-term outlook is positive.

Slides for the report in Lithuanian are available here

Returns on Lithuanian asset classes

| Asset class * | 1996-2022 average annual return, % | 2013-2022 average annual return, % | 2022 return, % |

| Rental housing (net of expenses starting in 2016) | 14.4 | 11.6 | 23.2 |

| Housing prices in Lithuania | 7.3 | 7 | 19.1 |

| Lithuanian stocks | 9 | 10.3 | -2 |

| Short-term Lithuanian debt securities and money market instruments (deposits) | 3.9 | 0.2 | 0.4 |

| Lithuanian long-term bonds | 4.2 | 4.8 | -8,4 |

| Lithuanian 2nd pillar pension funds | 4.8** | 4.8 | -13.8 |

| Inflation | 3.7 | 3.3 | 18.9 |

| Lithuanian Investment Index | 9.4 | 5.8 | 3.3 |

* Housing acquisition and rental returns calculated on the basis of Ober-Haus data.

** Since their creation in 2004.

For further questions about the Investment Index or additional comments from Vaidotas Rūkas, the head of INVL’s investment division, contact us by e-mail at media@invl.com.

The information provided herein shall not be construed as a recommendation, offer or invitation to invest in funds or other financial instruments managed by INVL Asset Management. When investing, you assume the investment risk. Investments can be profitable or unprofitable and you may not receive any financial benefit, or you may lose some or even all of the amount invested. Past performance of an investment does not guarantee future performance. In deciding whether to invest, you should assess all the risks associated with investing as well as the Key Investor Information documents. INVL Asset Management is not liable for any inaccuracies or changes in this information, nor for any losses that may arise when investments are made based on this information.

About INVL

INVL is the leading investment management and life insurance group in the Baltic region. Its companies manage pension and mutual funds and life insurance directions, individual portfolios, private equity, and other alternative investments. Over 300,000 clients in Lithuania, Latvia and Estonia and international investors have entrusted the group’s companies with the management of more than EUR 1.75 billion of assets. In the business for more than 30 years now, the group has solid experience in managing private equity assets and building market players that are leaders in their respective fields in the Baltic countries and Central and Eastern Europe.

![]()

INVL and Šiaulių bankas merged their retail services as of 1 December 2023.

Please select Your topic on SB.lt webpage.

![]()

INVL and Šiaulių bankas merged their retail services as of 1 December 2023.